Business

Sustaining monetary, fiscal policies for bank recapitalisation

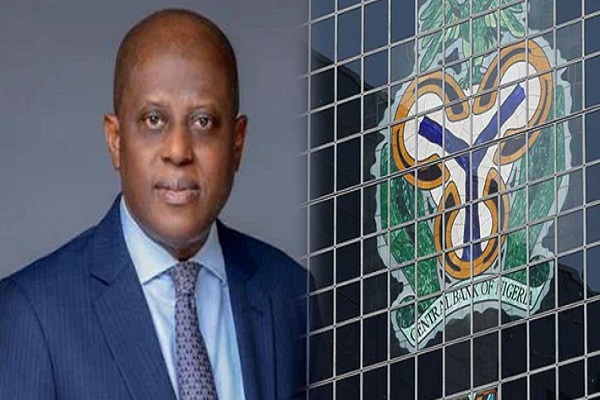

The emergence of stronger and bigger banks is one of the crucial benefits expected from the ongoing Central Bank of Nigeria (CBN)-led recapitalisation of banks. The apex bank believes that achieving sustainable economic growth requires strong support from the financial system. The financial sector regulator is, therefore, keen on aligning monetary and fiscal policies to achieve government’s vision of growth for businesses and $1 trillion economy size for the country, writes Assistant Editor, COLLINS NWEZE.

Aligning fiscal and monetary policy objectives comes with great benefits to the economy. The Central Bank of Nigeria (CBN) is at the centre of achieving fiscal and monetary policies collaboration and supporting the government’s plan for $1 trillion economy size.

For a government that wants to grow its economy to $1 trillion mark, the support of the financial services sector led by the Central Bank of Nigeria (CBN) Governor, Olayemi Cardoso is crucial.

The CBN boss had explained that bank recapitalisation ensures that lenders are well-capitalised, enabling them to take on greater risks, particularly in underserved markets. With stronger capital bases, banks can provide more loans and financial products to Micro Small and Medium Enterprises (MSMEs), rural communities and other vulnerable segments that have previously struggled to access formal financial services.

The CBN had, on March 28, 2024 announced a two-year bank recapitalisation exercise which commenced on April 1, 2024 and is expected to end on March 31, 2026.

The recapitalisation plan requires minimum capital of N500 billion, N200 billion and N50 billion for commercial banks with international, national and regional licenses respectively.

Others included merchant banks N50 billion; non-interest banks with national license N20 billion and non-interest banks with regional license will now have N10 billion minimum capital. The 24-month timeline for compliance ends on March 31, 2026.

Cardoso said the recapitalisation policy not only strengthens financial stability but also serves as a catalyst for inclusive growth.

“By enabling banks to extend more credit to MSMEs, we enhance job creation and productivity. Furthermore, with increased capital, banks can invest in technology and innovation, crucial for driving digital financial services such as mobile money and agent banking. These technologies are important to breaking down geographic and economic barriers, bringing financial services to even the most remote areas,” he stated.

He said Nigeria has what it takes to deepen financial inclusion and support the growth of business and economy. He said the recapitalisation exercise will also support the government’s efforts to achieve a $1 trillion economy.

The CBN further underscored the importance of banking recapitalisation as a major catalyst for the achievement of the $1 trillion economy agenda of the government.

Banking sector remains robust

Cardoso explained that the banking sector remains robust, with key indicators reflecting a resilient system.

“The non-performing loan ratio remains within the prudential benchmark of five per cent, showcasing strong credit risk management. The banking sector liquidity ratio comfortably exceeds the regulatory floor of 30 per cent, a level which ensures banks are maintaining adequate cash flow to meet the needs of customers and their operations. The recent stress test conducted also reaffirmed the continued strength of our banking system,” he said.

“I am pleased to note that a significant number of banks have raised the required capital through rights issues and public offerings well ahead of the 2026 deadline. I believe that the banking sector is in a strong position to support Nigeria’s economic recovery by enabling access to credit for MSMES and supporting investment in critical sectors of our economy,” he said.

The CBN Deputy Governor, Corporate Services, Ms. Emem Usoro, said the journey to a $1 trillion economy requires structured planning, clearly defined policies, unwavering implementation, and an inclusive approach that aligns public and private sector interests.

At the just-concluded seminar organised by the CBN for business editors and financial correspondents in Abuja, Usoro said that one of the key components of the $1 trillion ambition is the recapitalisation of Nigerian banks.

She noted that banks must be sufficiently capitalised to meet the financial demands of a larger and more dynamic economy.

“As we work towards building a $1 trillion dollar economy, we must consider the recapitalisation of our banks to be able to fund, finance and power the economy, and to favourably compete globally,” Usoro said.

She further called for a collective effort from all stakeholders, adding that the financial system must be prepared to play its role in powering development.

“We should particularly pay attention to bank recapitalisation to ensure that our banks are strong, resilient and stable enough to carry out financial intermediation, and the much-needed financing of development projects and programmes,” Usoro said.

The Group Managing Director of United Bank for Africa (UBA), Mr. Oliver Alawuba described the ongoing CBN bank recapitalisation policy as both timely and essential in positioning the financial system to meet the demands of a growing and globally competitive economy.

According to Alawuba, the initiative is expected to boost the resilience of the banking sector by strengthening its capacity to withstand economic shocks such as inflation, currency volatility and global geopolitical disruptions. He noted that the policy will also place Nigerian banks on a stronger footing to finance the country’s long-term economic transformation, including funding of large-scale infrastructure and industrial projects.

Alawuba further stressed that the recapitalisation policy goes beyond regulatory compliance. It is a forward-looking strategy aimed at equipping Nigerian banks to operate at the scale and sophistication required by a trillion-dollar economy. He said the move would enhance the sector’s ability to support traditional economic drivers such as oil and gas, agriculture and manufacturing, as well as emerging sectors such as fintech, green energy and infrastructure development.

“Nigerian banks need adequate capital buffers to meet the evolving demands of these sectors. Without this, the industry cannot effectively rise to the challenge,” he said.

Alawuba further pointed out the sharp contrast between Nigerian banks and their counterparts in more advanced economies, where bank assets typically range between 70 and 150 per cent of Gross Domestic Product (GDP). In Nigeria, bank assets accounted for just 11.97 per cent of GDP as of 2024, a gap he said must be addressed if the country’s financial system is to align with international standards.

He commended the CBN’s recent directive mandating a significant increase in minimum capital thresholds, describing it as recognition of the urgent need for stronger financial institutions capable of delivering on national priorities such as infrastructure expansion, digital transformation, inclusive financial services and economic diversification.

Alawuba concluded that a robust, well-capitalised banking sector is critical for Nigeria’s aspiration to become a one trillion-dollar economy, and the recapitalisation drive is a forward-looking step to achieve that goal.

According to the Director of the Banking Supervision Department at the CBN, Olubuka Akinwunmi provided insights into the state of the banking sector by stating that banks have so far remained within the prudential thresholds stipulated by the regulator, including benchmarks for capital adequacy ratio and non-performing loans.

“Currently, all our banks are still within the prudential thresholds that were set. And they are actively pursuing various recapitalisation efforts,” Akinwunmi said.

He said priority sectors such as agriculture, infrastructure and manufacturing are receiving attention from both the government and financial institutions, as they are crucial to achieving a trillion-dollar economy.

“This year’s national budget reflects a clear emphasis on critical sectors such as health, education, infrastructure and agriculture. Banks are taking cues from these priorities, recognising them as viable areas for business expansion,” Akinwunmi said.

On how many internationally-active banks had met the new N500 billion capital requirement, he noted that substantial progress has already been made.

“We are halfway through the journey in terms of timeline, and in terms of capital already raised; we are also halfway through. That is a positive signal,” he said.

He added that the decision to start the recapitalisation process early has helped insulate the financial system from emerging global and domestic shocks.

“The emerging global economic shifts and pressures were not lost on the management of the CBN. We started early. If we had waited till now, the challenges would have been greater. But we acted in time,” he stated.

Dr Akinwunmi expressed his confidence that the recapitalisation requirements will be met, stressing that existing shareholders’ funds continue to serve as a buffer. However, the CBN deliberately opted for fresh capital inflows, particularly from foreign investors who have shown renewed confidence in Nigeria’s financial system.

“International perception of Nigeria’s banking sector is improving. The reforms over the past year, especially around the foreign exchange regime and improved transparency regarding reserves, have improved investors’ confidence,” he said.

He cited recent disclosures on Nigeria’s net reserves and improvements in regulatory credibility as key factors that are reshaping the outlook for foreign direct investment in the banking sector.

On the Loan to Deposit Ratio (LDR), Akinwunmi explained that the current 50 per cent benchmark does not reflect a reluctance to lend but rather a contextual response to inflation and other macroeconomic challenges.

“As the macro-economic environment stabilises, banks will naturally increase lending. It’s a cautious approach to ensure that lending supports sustainable growth,” he said.

He also touched on the Cash Reserve Ratio (CRR), stating that there has been marked improvement in transparency. Banks now have a clearer understanding of CRR computations, unlike in the past, which enhances predictability and compliance.

On Small and Medium Enterprises (SME) funding, he confirmed that banks have continued to make provisions, but the CBN remains actively engaged to ensure proper disbursement and sectorial targeting. Supervisory oversight, he explained, is being deployed to verify compliance and effectiveness of disbursed funds.

On incentives, he said the most powerful incentive for banks lay in the opportunities provided by a growing economy.

“A stronger bank can take on big-ticket businesses, including infrastructure financing. The current reforms, such as the infrastructure concession plans, present viable business opportunities for well-capitalised banks,” Akinwunmi said.

The capital verification process, according to him, is thorough and designed to ensure that only legitimate, unborrowed funds are used for recapitalisation. An industry-wide tracking mechanism has been established to streamline verification across institutions and enhance collaboration.

“Our examiners follow each capital trail meticulously, moving from one bank to another as necessary. Even if it’s not your bank under verification at that moment, we expect full cooperation to trace the sources of capital,” he said.

On the broader question of resilience to global shocks, he maintained that Nigerian banks are being positioned to remain attractive to investors and capable of withstanding external disruptions.

“CBN is monitoring developments closely and adjusting where necessary. The recapitalisation process is not just about compliance — it’s about long-term stability, competitiveness and economic transformation,” he said.

The Trade Union of Nigeria, TUC, has raised the alarm that the price of Premium Motor Spirit aka Petrol may climb to about N2,000 per litre if urgent measures are not taken to cushion the impact of rising global crude prices and the depreciating naira.

Speaking to newsmen on Thursday, April 9, the president of the TUC, Festus Osifo, called on the Federal Government to immediately deploy 60 percent of excess crude oil revenue above the 2026 budget benchmark to subsidise crude feedstock supplies to the Dangote Refinery and other modular refineries, a move it says will slash pump prices of petrol, diesel, and jet fuel within two weeks

“Today, comrades, we are seeing that the cost of petrol is edging towards N2,000 per litre depending on the part of the country that you are. Nigerian workers are already passing through excruciating pain as we speak.

The same way it is affecting transportation, it is also affecting manufacturing. The cost of diesel has also gone northward, meaning that the cost of production has increased. When production costs rise, the final price of goods on the shelves will also skyrocket.

If this continues unchecked, the inflation that we are currently celebrating as going downwards will reverse and start moving up again,” he stated.

Osifo outlined the proposal as an urgent intervention to cushion Nigerian workers from excruciating pain caused by petrol prices edging towards ₦2,000 per litre in some parts of the country

The governor of Oyo state, Seyi Makinde, has approved a N10,000 transportation allowance as a palliative for the state workforce to cushion the effects of the increase in the pump price of Premium Motor Spirit, otherwise known as petrol.

The Chairman of the Nigeria Labour Congress (NLC), Oyo State chapter, Kayode Martins, in a statement released on Monday, March 23, disclosed that the governor has granted the request of the union on the issue of transportation allowance.

The statement read

“Following the intervention and formal request made by the State Council of the Nigeria Labour Congress (NLC) earlier this morning, the state government has approved a N10,000 transportation allowance for all workers in the state.

The newly approved allowance is set to take effect from April 2026, providing much-needed relief to workers grappling with rising transportation costs amid current economic challenges.

This development comes as a direct response to sustained advocacy by the state NLC, aimed at cushioning the impact of increased living expenses on the workforce.

Further details on implementation are expected to be communicated by the relevant government authorities in due course.”

The Central Bank of Nigeria (CBN), has declared that banks and financial institutions must establish and maintain a temporary watch-list for Bank Verification Numbers (BVN) implicated in suspected fraudulent transactions.

According to the CBN in a circular dated March 12, 2026 and signed by its Director of Payments System Policy Department, Musa I. Jimoh, the apex bank said such a suspected BVN may remain on the temporary watchlist for a maximum period of twenty-four (24) hours during which the owner would be contacted to make clarifications.

The circular explained that the move is part of several new measures under a revised regulatory framework aimed at enhancing financial system stability.

“A BVN may remain on this temporary Watchlist for a maximum period of twenty-four (24) hours, during this period, the BVN owner shall be contacted to provide clarification regarding the identified transaction(s),” the circular stated.

The circular also sets an age requirement for BVN enrolment, restricting registration to individuals who have attained eighteen (18) years and above.

The CBN also added that amendments to phone numbers linked to a BVN shall be allowed only once.

“Amendments to phone numbers linked to a BVN shall be allowed only once,” the circular noted.

The apex bank stated that access to BVN databases will remain tightly controlled.

“Access to the BVN databases shall be exclusively granted to Central Bank of Nigeria (CBN) licensed financial institutions.

“Notwithstanding this provision, the Central Bank of Nigeria (the Bank) reserves the right to approve access to the BVN databases in extenuating circumstances and in accordance with the provisions of extant laws,” the circular said.

Financial institutions are expected to comply with the new requirements, and customers may be contacted by their banks if their BVNs are temporarily flagged during the new fraud monitoring process.

The new policy, as stated by the CBN, takes effect from May 1, 2026.

2027: More Than 50 Lawmakers Lose APC Reps Tickets in Major Primary Election

Bandits behind Ogbomoso school abduction will face full wrath of the law- President Tinubu

PDP to screen Goodluck Jonathan on Tuesday as its sole Presidential aspirant For 2027 race

-

Business2 years ago

US court acquits Air Peace boss, slams Mayfield $4000 fine

-

Trending2 years ago

Trending2 years agoNYA demands release of ‘abducted’ Imo chairman, preaches good governance

-

Politics2 years ago

Politics2 years agoMexico’s new president causes concern just weeks before the US elections

-

Politics2 years ago

Politics2 years agoPutin invites 20 world leaders

-

Politics2 years ago

Politics2 years agoRussia bans imports of agro-products from Kazakhstan after refusal to join BRICS

-

Entertainment2 years ago

Bobrisky falls ill in police custody, rushed to hospital

-

Entertainment2 years ago

Bobrisky transferred from Immigration to FCID, spends night behind bars

-

Education2 years ago

GOVERNOR FUBARA APPOINTS COUNCIL MEMBERS FOR KEN SARO-WIWA POLYTECHNIC BORI